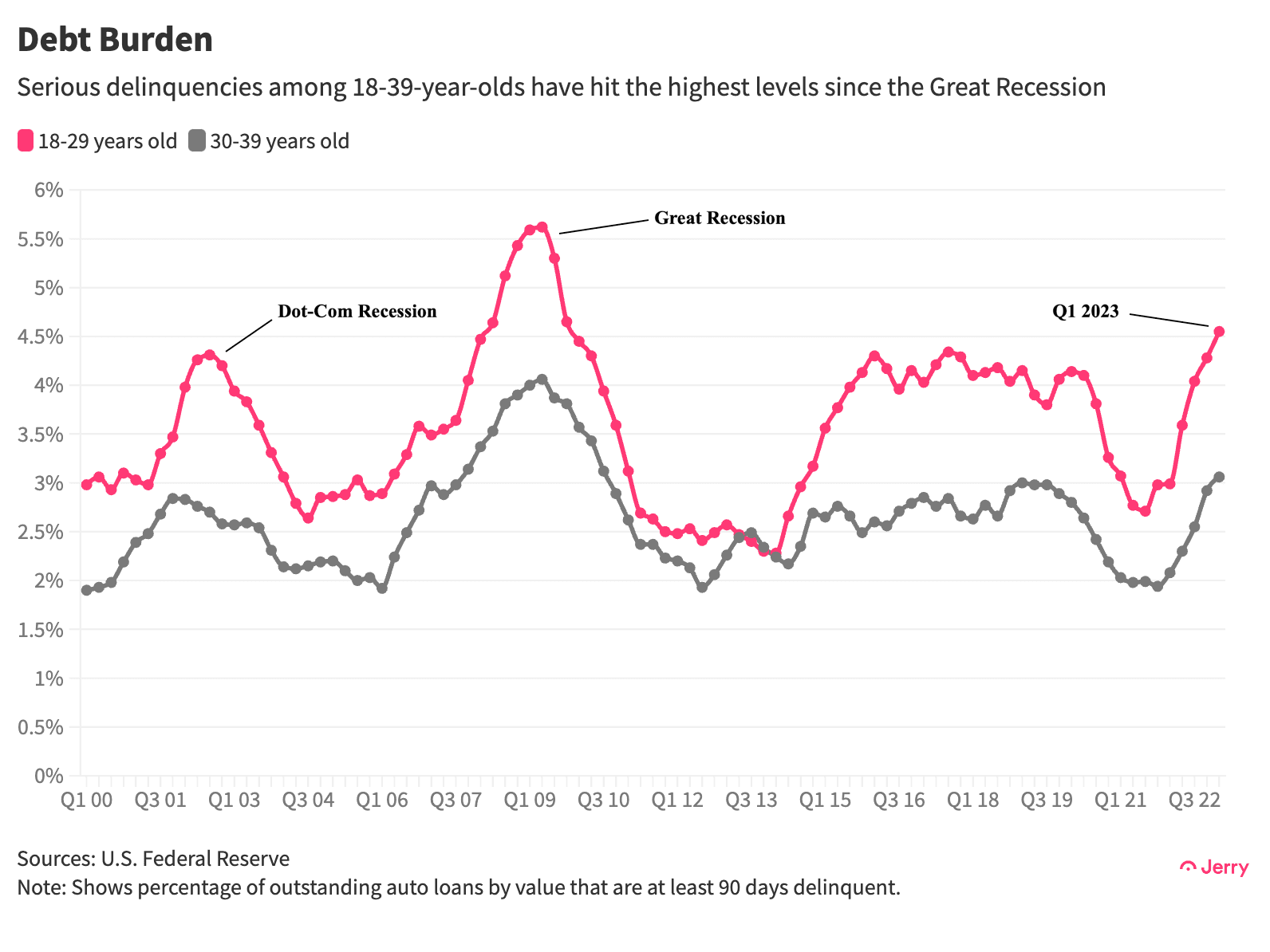

to a degree not seen since the global financial crisis more than a decade ago.

Generation Z and Millennials fell into serious delinquency (90+ days past due) on about $20 billion in auto loans during the 12 months through March this year, according to the Federal Reserve’s

Jerry’s analysis of the Fed data offers further evidence that surging costs of car ownership have been especially punishing for younger generations, particularly members of Gen Z, who binged on auto loans after COVID-19 hit the U.S. in early 2020.

Key Insights

For Gen Z and Millennials, serious delinquencies in auto loans in the 12 months through March hit the highest level in more than a decade. Among 18-29-year-olds, they reached the most since 2009; for 30-39-year-olds, the highest since 2010.

Together, drivers aged 18-39 accounted for about $20 billion in auto loans that fell into serious delinquency during the four quarters that ended March 31 this year.

Delinquencies are also rising at a blistering pace. For borrowers 18-29 years old, serious delinquencies rose the most on record for any four-quarter period in data going back to 2000. For those aged 30-39, the jump was the biggest since 2007.

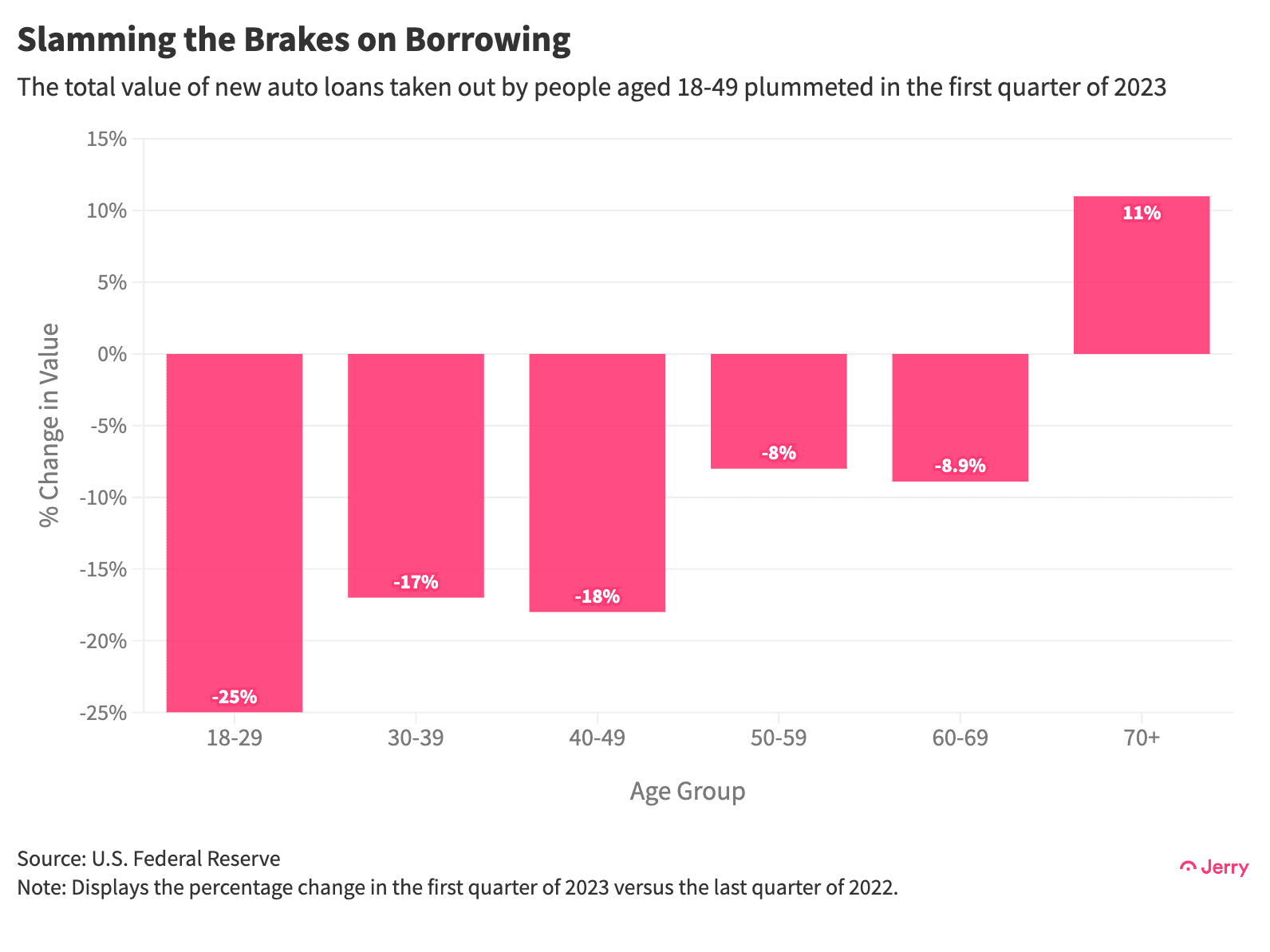

The surge in delinquencies coincides, perhaps not surprisingly, with a steep drop in new auto loans, particularly among borrowers with lower credit scores. The value of new auto loans taken out during the first quarter of this year by borrowers aged 18-29 dropped 25%, the most on record in data going back to 2000. For borrowers aged 30-39, the value of new auto loans fell 17%, the most since 2005.

Slightly older borrowers have also seen a jump in delinquencies, though to a lesser degree, and a plunge in new auto loans. For those aged 40-49, serious delinquencies over the past four quarters rose the most since 2009, while new auto loans fell in the first quarter of this year by the most since 2005.

Feeling the Pain

Rising costs of car ownership—including vehicle prices, maintenance and repair costs, and

premiums—have fallen hardest on younger drivers, who generally earn less money and have less savings to fall back on in tough times than their older counterparts.

Consider that while nearly a third (29%) of American vehicle owners say

forced them to take on debt at some point in the past two years, nearly half (46%) of Gen Z drivers and well over a third (38%) of Millennials said this was true of themselves.

Similarly, 19% of Gen Z drivers and 12% of Millennials say repair costs caused them to default on a car loan in the past three years, compared with 6% of all American vehicle owners.

Pulling Back

Nearly every generation took out far fewer auto loans during the first three months of this year. This is perhaps unsurprising, as it follows two years of painful inflation for everything from vehicles to eggs, and a resulting jump in U.S. interest rates, and comes at a time of growing economic uncertainty.

Again, younger generations led the way—much as they did in borrowing over the previous couple of years. The value of new auto loans taken out by Gen Z fell 25%, while the number was 8%-9% for those aged 50-69. New loans taken out by those aged 70+ actually rose 11%.

But this downshifting may be due to lenders tightening credit standards as much as beleaguered borrowers hesitating to take on debt. For all age groups, new auto loans taken out by people with credit scores below 660 fell 19.4% during the quarter, compared with a 7.7% drop for those with scores of 660 or above, the Fed data showed.

This is a continuation of a years-long trend. In 2018, so-called subprime and deep subprime borrowers accounted for 24% of all new auto loans, but the number fell to 16% in the first quarter of 2023, according to Experian.

Conclusion

Despite the economy holding up pretty well, younger borrowers are struggling to stay afloat on auto loans as the

in car ownership costs outpace overall inflation. With many economists seeing a recession on the horizon, delinquency and default rates could climb even higher, wrecking credit histories and bank balance sheets in the process.

Methodology

The age groups chosen by the Fed for the auto lending and loan delinquency data in this study do not perfectly align with the

of Gen Z and Millennials as defined by the Pew Research Center. (The oldest members of Gen Z, according to Pew, turn 26 in 2023, while Millennials would be 27-42.) However, as Pew noted, choosing the years in which to divide generations isn’t an exact science either.