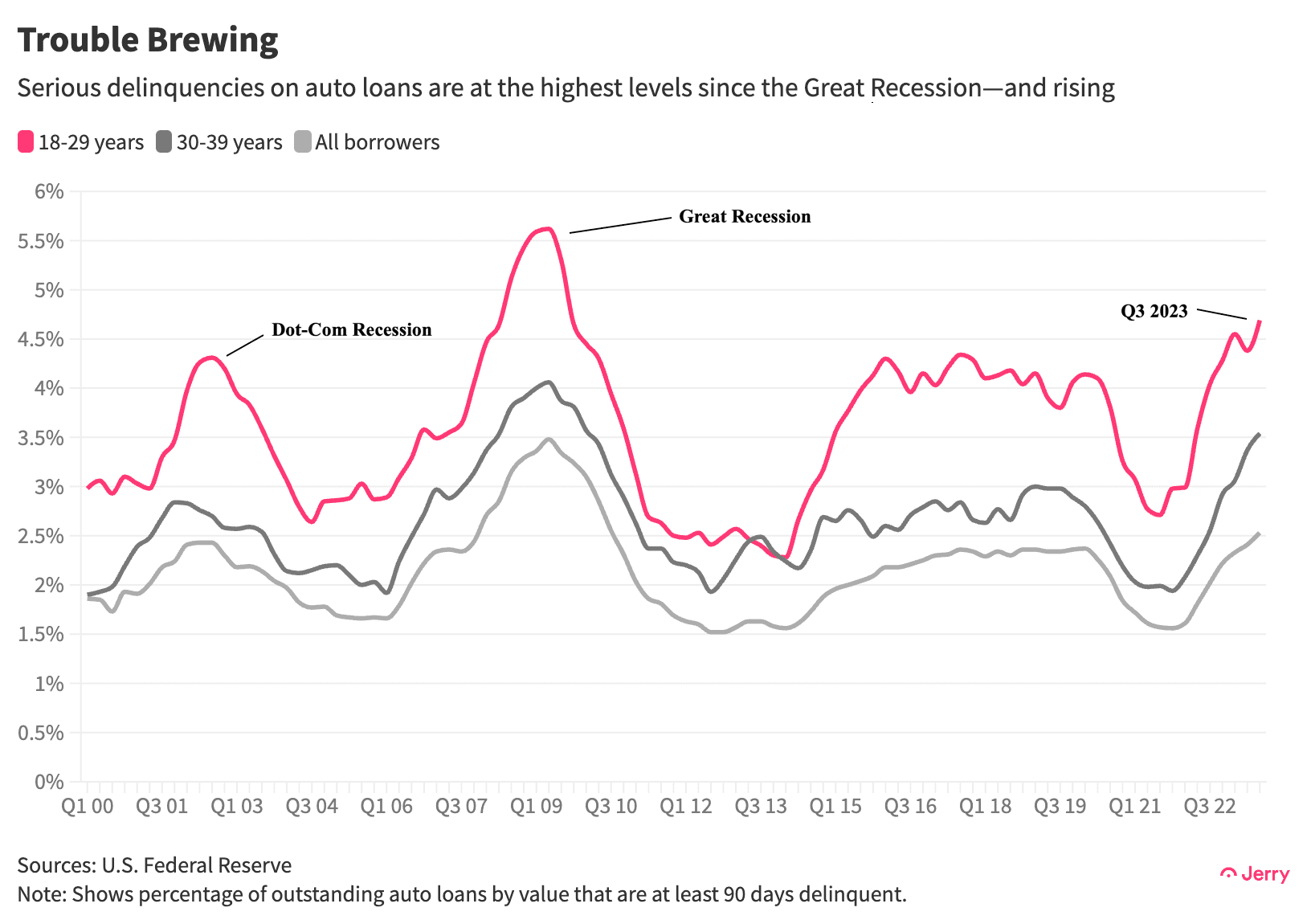

Young Americans fell behind on their car loans during the third quarter at rates not seen since the Great Recession, as several years of soaring car-ownership costs and interest rates take a growing toll on their personal finances.

For Gen Z and Millennials, serious delinquencies—defined as 90 or more days late—have reached the highest levels since 2009 and 2010, respectively, just as the three-year moratorium on student loan payments comes to an end.

But they aren’t quite alone. Older borrowers are starting to miss payments, too, with serious delinquencies among the 40-59 age group reaching levels not seen since the early days of the COVID-19 pandemic.

Key Insights

In the third quarter of 2023, serious delinquencies (90+ days late) among borrowers aged 18-29 have hit the highest level since 2009, in the immediate aftermath of the global financial crisis, while those among borrowers aged 30-39 have reached the highest since 2010.

Serious delinquencies among those aged 40-59 have reached the highest level since the second quarter of 2020, the early days of the COVID-19 pandemic.

The rise in early delinquencies (30+ days late) signals more trouble is likely on the way. Early delinquencies among all borrowers hit the highest level since 2017 during the third quarter.

The rise in auto loan delinquencies underscores Americans’ struggle to cope with

at an annual rate of 19% in September, the fastest pace in at least four decades. While the rise in new vehicle prices has slowed, they’ve still jumped 23% over the past four years. Used vehicles remain 35% more expensive than four years earlier, even after price declines in the past two years.

The struggle to keep up just got harder for those with student loans. The federal government’s suspension of student loan payments as part of COVID relief has ended, with payments resuming in October after a pause of more than three years.

That isn’t expected to deliver a big blow to the broader economy, but it will certainly add to the burden on many individual households. The total household debt balance hit $17.3 trillion in the third quarter of this year, up 4.8% from a year earlier and 21% since the first quarter of 2020, when COVID struck.

That could mean more missed car payments, although student loans generally are lower on the repayment hierarchy than car loans, with mortgages at the top. Still, lenders who had overlooked student loans during the repayment moratorium are sure to stop that practice, meaning approval rates for car loans and other loans may drop. Lenders had already tightened standards on car loans in recent years,

Methodology

All delinquency and debt data is drawn from the U.S. Federal Reserve’s Quarterly Report on Household Debt and Credit. Car-ownership inflation data is from the U.S. Bureau of Labor Statistics.