Serious delinquencies in auto loans — defined as behind on payments by 90 days or more — jumped the most since the 2008-09 Global Financial Crisis in the third quarter of 2022, after an increase almost as big the previous quarter, according to the latest data from the U.S. Federal Reserve. For those under 30, serious delinquencies have jumped more in the past two quarters than in any other six-month period on record in data going back to 2000.

Younger people and those earning lower incomes say they expect to struggle to make payments in the months ahead. Those under 40 and those earning under $50,000 a year said there was nearly a one-in-five chance they would miss a minimum debt payment of some sort over the next three months, according to a Fed

in September. That was the strongest expectation of debt delinquency for people under 40 since the spring of 2020, when 14 million people lost their jobs during the first COVID-related shutdowns.

Though overall delinquencies on car loans remain below the levels that were ringing

in 2019, they are nearing those levels and rising quickly at a time when employment and financial conditions are likely to get worse for many borrowers.

Key Insights

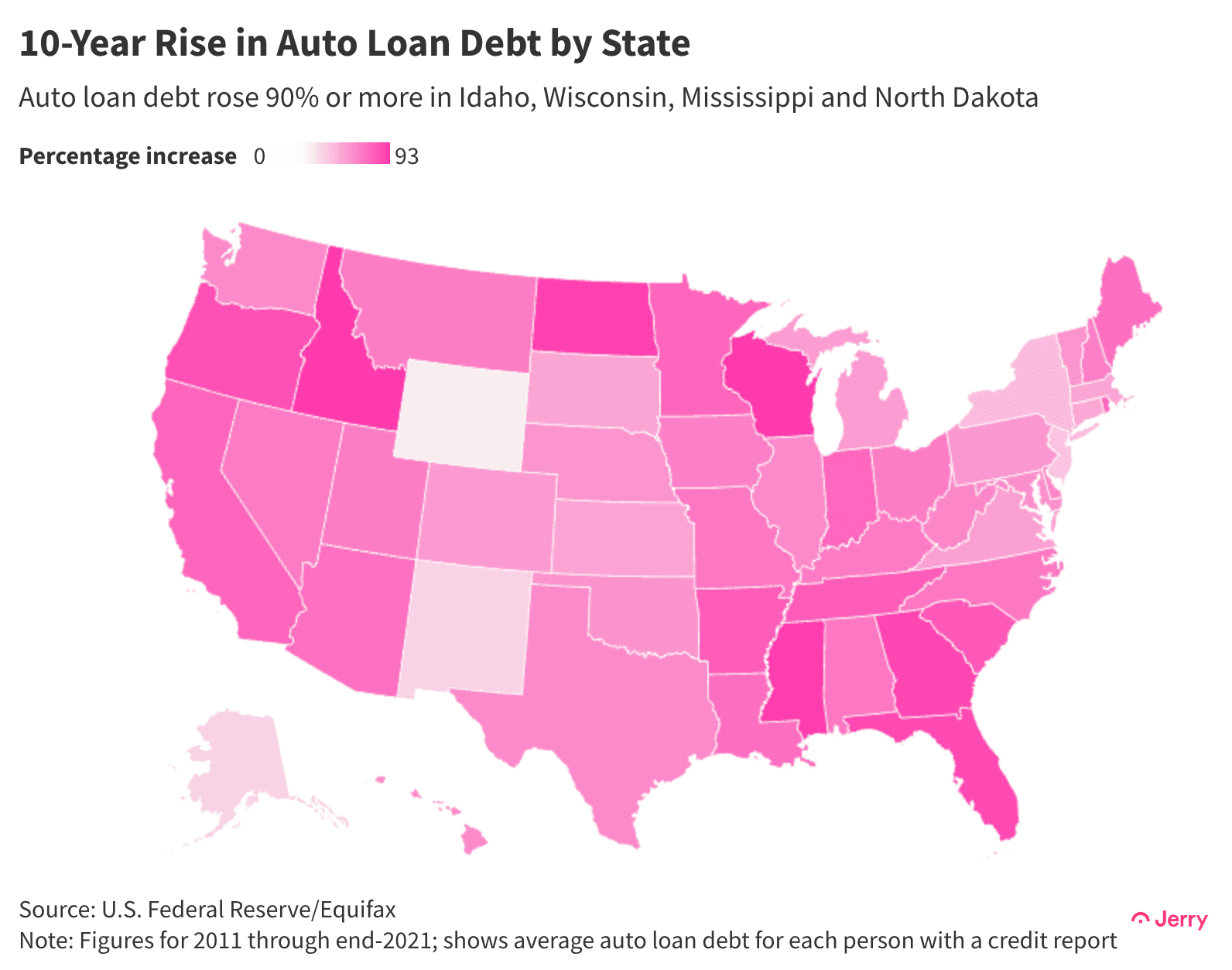

Serious delinquencies in car loans rose the most since the Global Financial Crisis in the third quarter of 2022, with roughly $3.2 billion worth joining the 90+ days-late category. For borrowers under 30 years old, serious delinquencies reached pre-pandemic levels.

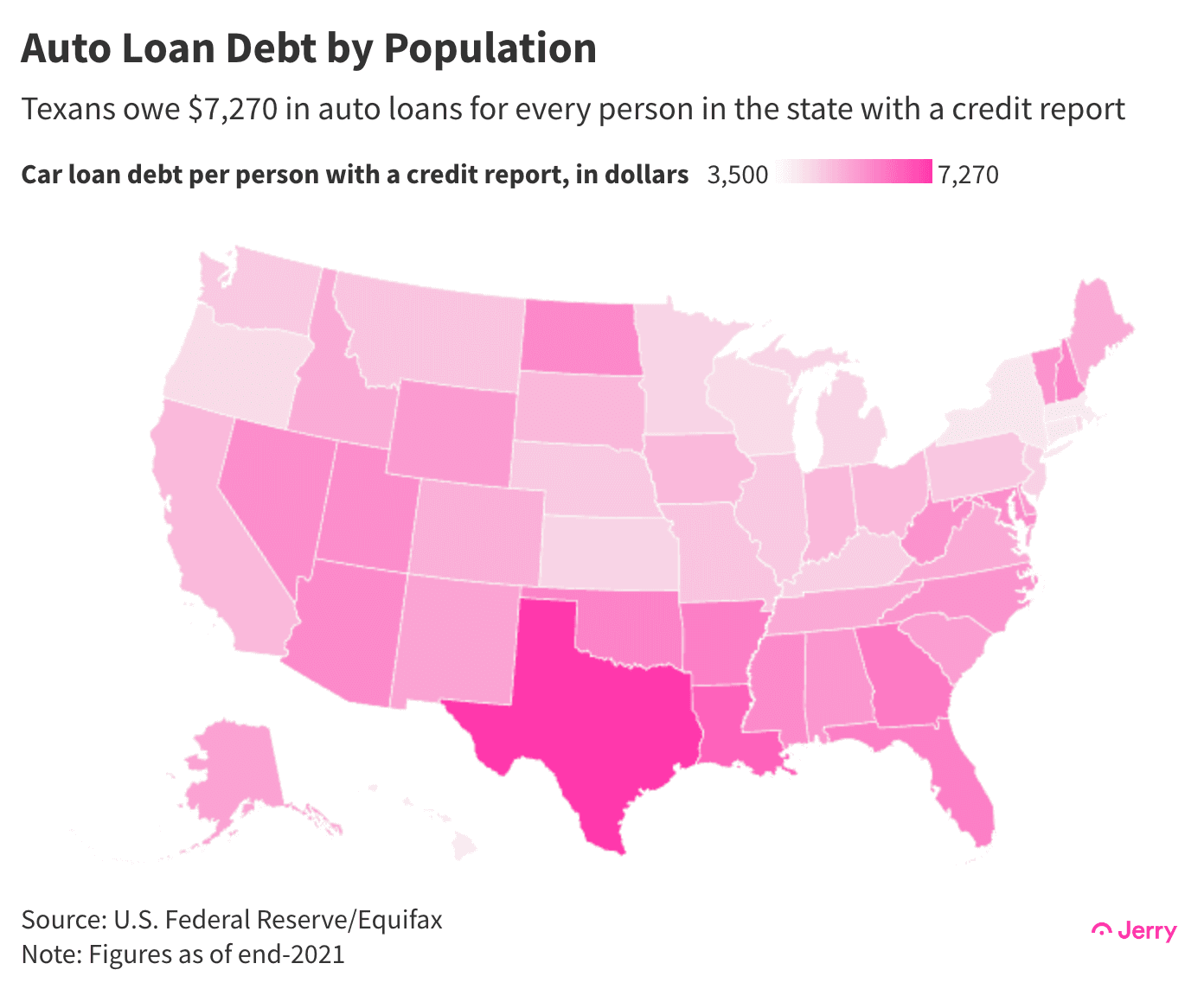

There was $4,600 in car loan debt for every single American at the end of September.

A couple earning the median household income for married couples would pay 16% of their after-tax income on payments for two new cars at average loan values. One used and one new vehicle would cost them 14% of their take-home pay.

The average single woman living alone would pay 23% of her after-tax income on payments for an average new car loan and 17% for a used one. A single man would pay 18% for a new vehicle and 13% for a used one.

Car Loans Binge

Americans are loaded up on auto loans like never before. At the end of September this year, the total value outstanding nationwide was $1.52 trillion, double the amount 10 years ago. Put another way, auto loan debt totaled $4,600 for every person in the country.

At the state level, Texas led the way in auto loan debt by population. According to the Fed, each person in Texas with a credit report owed an average of $7,300 in car loans at the end of 2021. Texas was followed by Louisiana ($6,500) and Georgia ($6,100).

The value of borrowing has sped up sharply in the past few years as surging prices for new and used cars led people to take out ever-bigger loans. The average new car loan hit $38,000 in the second quarter of this year, an increase of 22% over three years, according to the latest available data from the Fed. For used cars, it was $25,000, up from $18,000 three years earlier.

This has stretched many household budgets — for some, to near or past the breaking point. Financial advisers say your car payment should eat up no more than 10%-15% of your take-home pay. Staying under that threshold has become a challenge for most.

A couple earning the median household income for married couples ($96,000 after taxes, according to the U.S. Census Bureau) would pay 16% of their after-tax income for two new cars. One used and one new vehicle would cost them 14% of their take-home pay. (These figures don’t include additional costs such as

A single mother would pay 15% of her take-home pay for a loan on an average new car and 11% for a used one. A single woman living alone would pay 23% of her after-tax income on a new car and 17% for an average used one.

Recession Looms

In its quest to vanquish inflation, the Fed is determined to squash consumer demand with its interest-rate hikes. Most economists now see a recession as highly likely if not a certainty. That will mean millions of people losing their jobs and millions more earning less than before, making it difficult or impossible to keep up with their car payments.

Delinquencies on car loans taken out in 2021 and 2022 are already slightly higher than on loans taken out in previous years, according to the Consumer Financial Protection Bureau (CFPB). Given the surge in car prices and loan values over the past two years, and many repayment periods being stretched to six years and longer, some households will face “increased pressure” on their budgets for much of the next decade, according to the CFPB.

Those who took out car loans in the past two years are likely to face the added challenge of

in the value of their cars as the market returns to normal or something like it. That means many of those borrowers could find themselves underwater on their loans — owing many more thousands of dollars than their vehicles are worth. That wouldn’t just be bad news for them. It could be bad for their lenders because borrowers might be more likely to walk away from the loan.

Under Stress

Young people, people who make less money and those with bad credit will face the biggest challenges — and conversely, pose the biggest risk to lenders and the economy — as the Fed continues its mission.

It was delinquencies among those with bad credit — so-called subprime borrowers — that were raising the most alarms in 2019, before COVID-related stimulus payments and debt forbearance helped fend off a possible wave of defaults. Banks and finance companies responded to the pre-COVID rise in delinquencies by

, squeezing many subprime borrowers out of the market over the past two years.

Those tighter standards may help prevent or limit any wave of defaults ahead. But those subprime borrowers who still managed to secure car loans saw the prices they paid for vehicles, their loan values and their monthly payments rise even more steeply than borrowers with good credit, according to Experian. That could mean a higher risk of trouble ahead.

Some relief is available, though, for subprime borrowers, who generally pay much higher interest rates than people with higher credit scores. They can still refinance their car loans despite the Fed’s continuing rate hikes.

“If you bought your car from a dealership, and especially a ‘buy here, pay here’ lot, there’s a very high probability that you can get a lower interest rate and payment by refinancing your auto loan,” said Lynda Vittes, senior director of auto finance at Jerry. “We’re seeing Jerry auto refinancing customers reduce their interest rate by more than five percentage points.”

Methodology

To calculate the percentage of take-home pay required to make loan payments on new vehicles, Jerry used Census Bureau data on after-tax median household incomes for 2021, Federal Reserve Bank of New York’s data on the average value of new car loans, and the average interest rate (5%) and loan maturity (66 months) on new car loans at finance companies as of August 2022.

For used vehicles, we used Fed data on the average value of used car loans, Experian data on average interest rate on used car loans (8.62%) in the second quarter, and Fed data on the average maturity of used car loans issued by finance companies in the second quarter (66 months).

To calculate the auto loan debt per capita in the U.S., we used the Census Bureau’s current estimate for the national population and the Fed’s figure for total outstanding auto loan debt at the end of the third quarter of 2022. For state figures on auto loan debt by population, we used Fed calculations, which divided total auto loan debt by the number of people with a credit report.