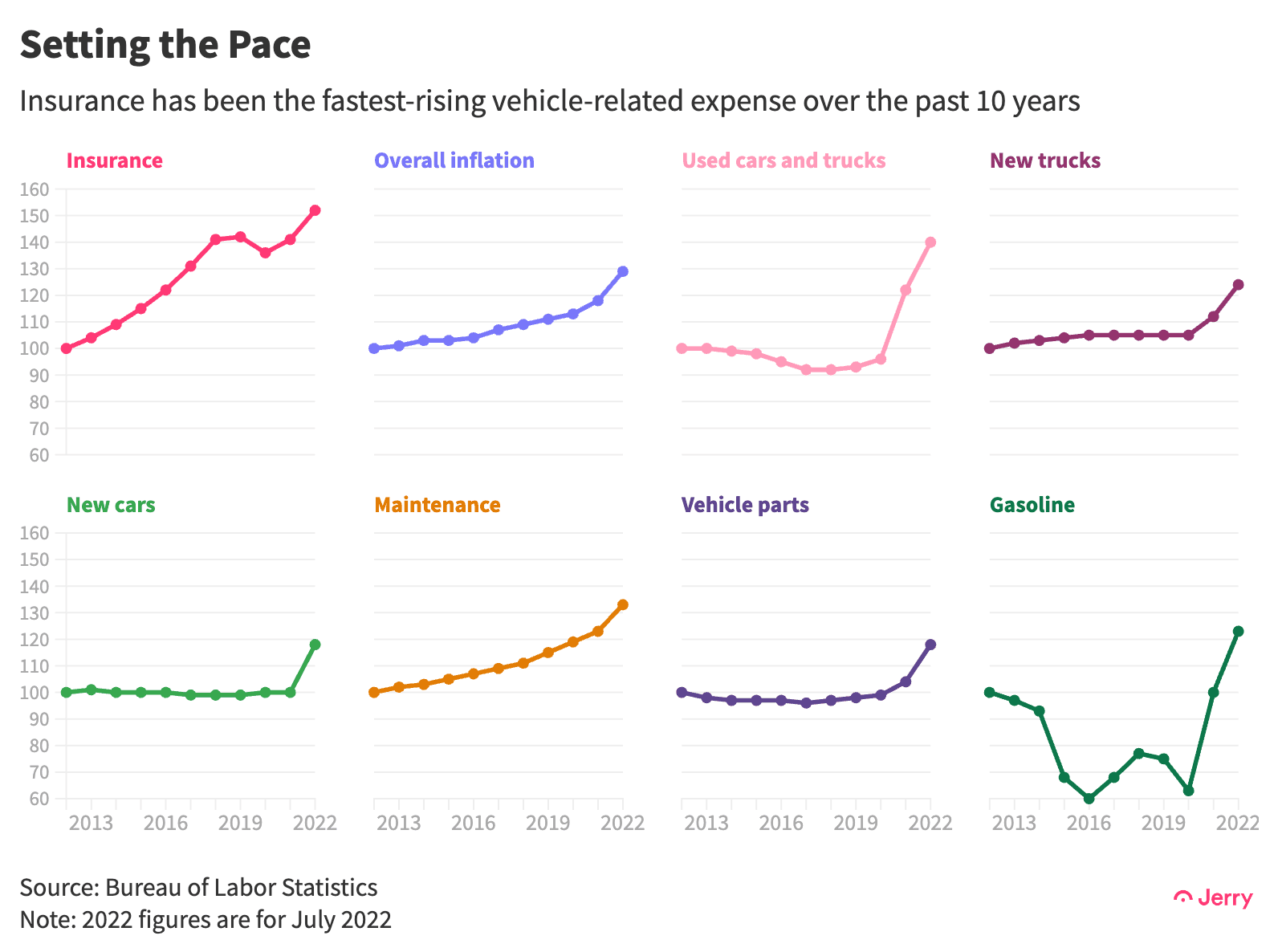

still ranks as the fastest-rising major vehicle-related expense over the past 10 years, eating up a growing share of American household expenses.

As of August, premiums were up 9.5% in 2022, accounting for about 3% of all spending by households earning $35,000 to $60,000 a year, according to data analysis by

. That’s more than double what those households spend on prescription and over-the-counter drugs combined, and 51%-73% more than they spend on vehicle maintenance and repairs.

Key Insights

Insurance was the fastest-climbing vehicle expense from 2012 through July 2022, increasing 52% despite insurers offering discounts during the COVID-19 shutdowns in 2020, according to

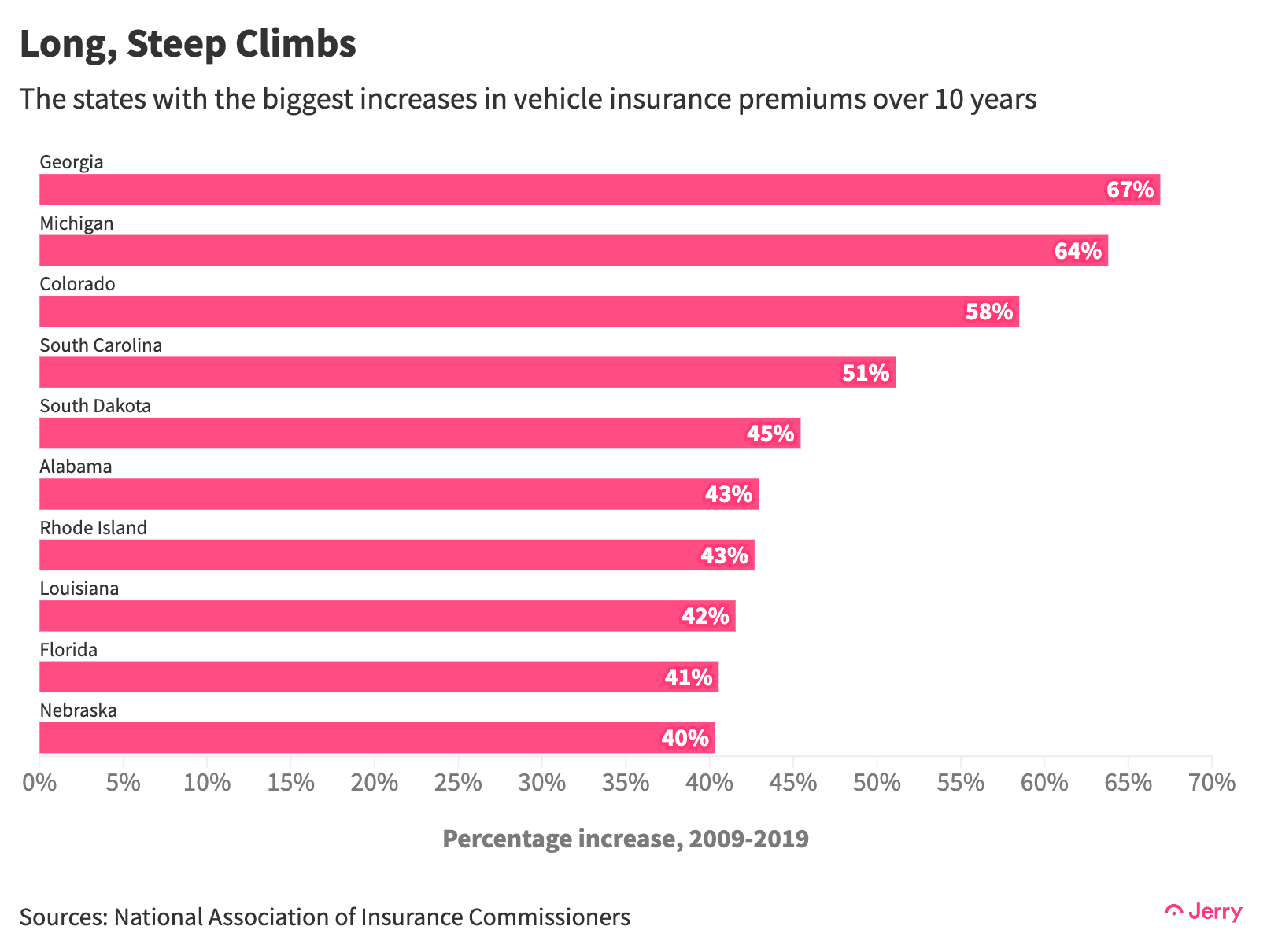

In 10 states, the average premium exceeded 2% of the median household income in 2019, the latest year for which state-level premium data were available from the

saw the biggest increases from 2009 to 2019. More than half of all states saw premiums rise at least 30% over 10 years, and 15 saw them jump at least 20% over the previous five years.

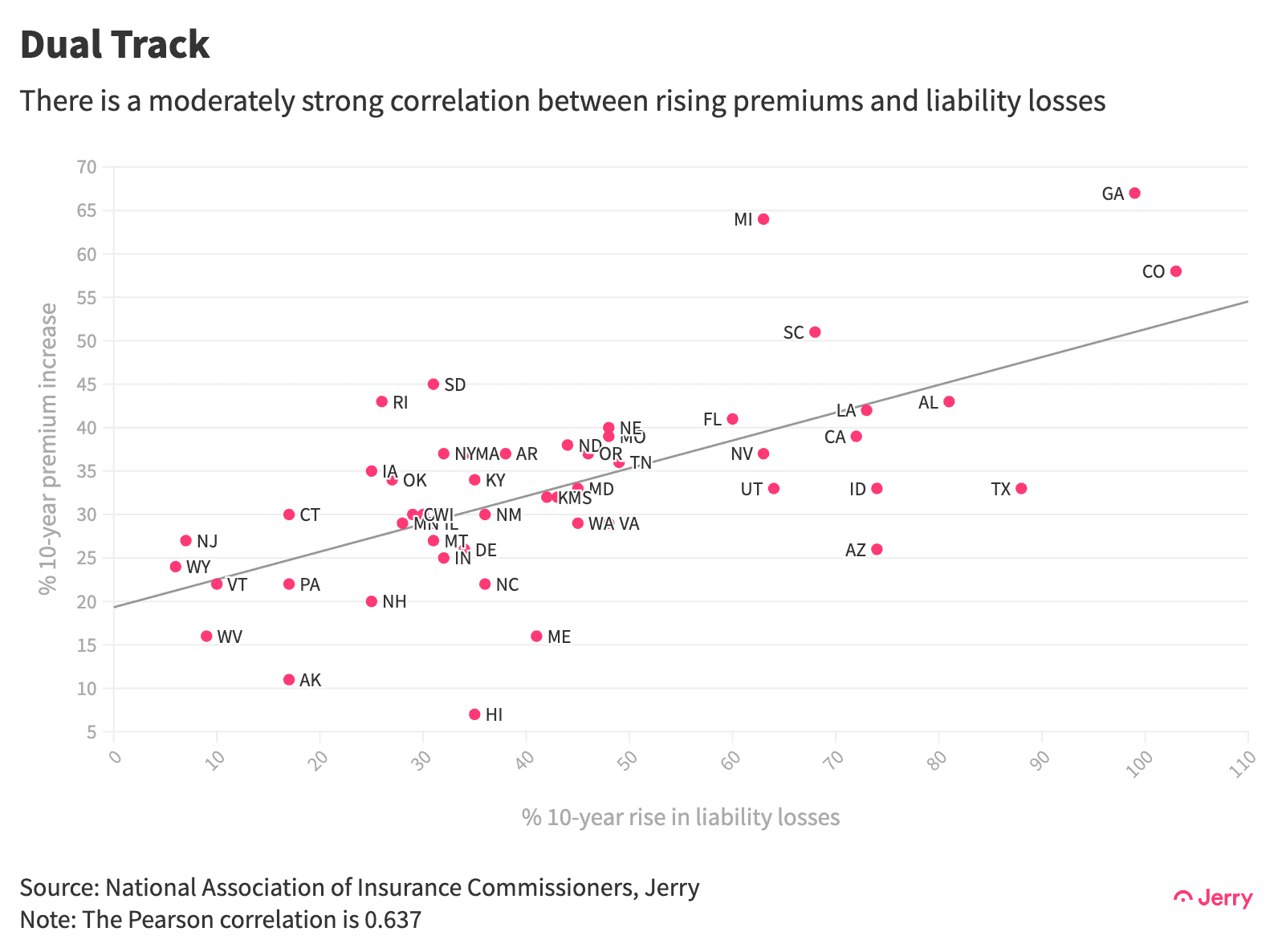

The cost of insurance claims has also been soaring. Total incurred losses from private and commercial auto insurance nationwide rose 53% from 2012 through 2019, when they totaled $185 billion. In the same time span, the average premium nationwide rose 42%.

Soaring auto insurance premiums and the question of their affordability have attracted the attention of

. It’s easy to see why. Consider that premiums in Georgia, for example, rose 67% from 2009 to 2019, according to data from the NAIC. Georgia suffered the steepest increase of any state, but it wasn’t alone in feeling the pain. Michigan was close behind and Colorado not far back.

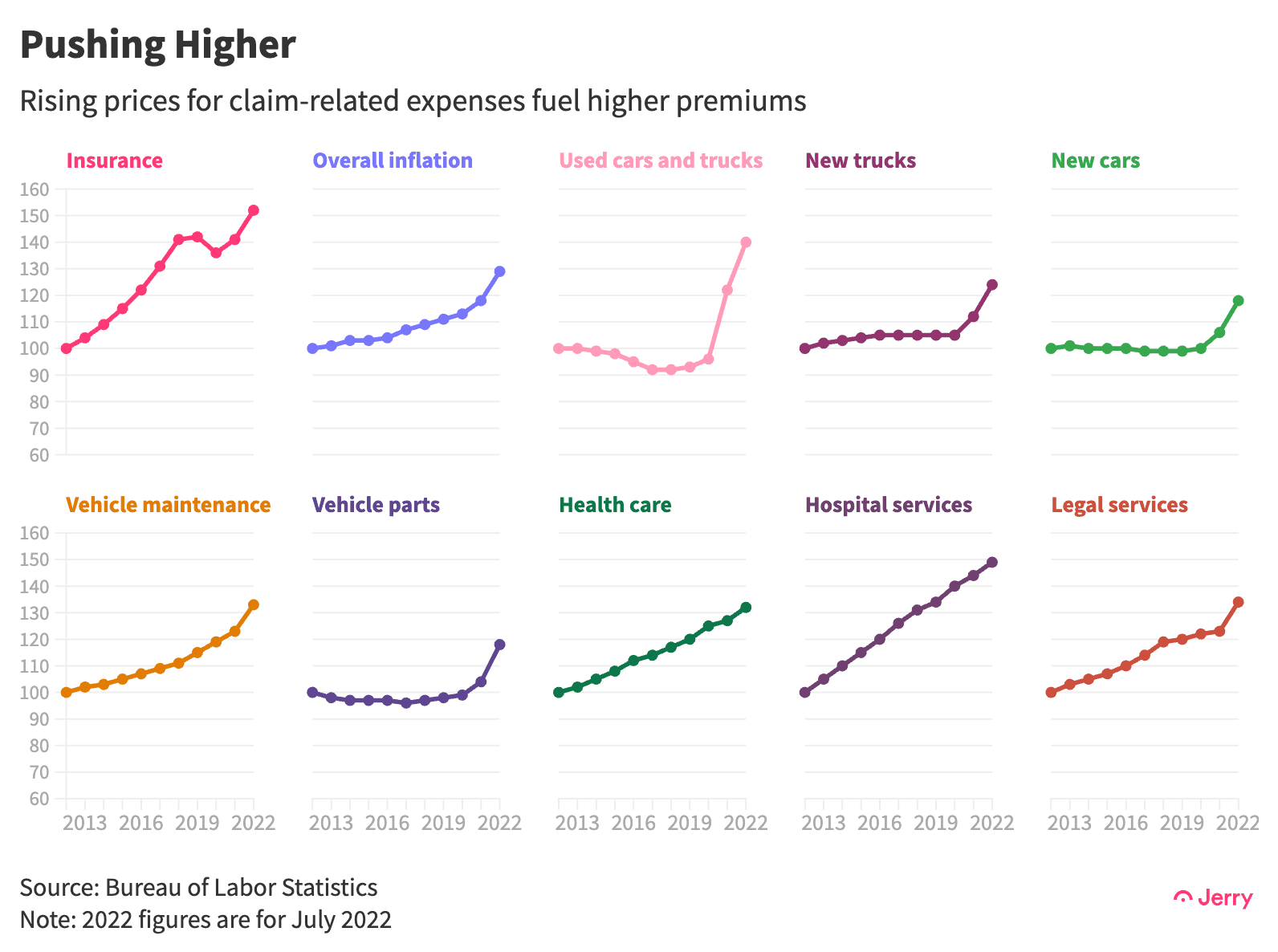

Insurance companies say the bottom line is that losses from claims are also soaring, forcing them to raise premiums or

. Surging prices for hospital stays, legal fees, auto parts, vehicle maintenance and, more recently, vehicles themselves are all factors in any rate hikes, the companies say. They also point to more frequent and

The recent spike in prices for used and new vehicles means insurance carriers have to pay more anytime a vehicle is destroyed in a crash or stolen, according to Josh Damico, vice president of insurance operations at Jerry.

“And when a car in an accident is repairable, it costs significantly more to repair,” Damico said. “Car parts are in high demand and they cost more, and body shops can’t find enough mechanics to hire, driving up the cost of labor. All of these factors drive up expenses in the case of an accident or vehicle theft, which can cause insurance premiums to rise.”

Auto insurance is highly regulated at the state level and any rate increase must be approved by the state. To be granted an increase, the insurance companies generally must provide data, submitted via independent statistical agents, showing the hike is justified. That data includes losses from claims as well as operating expenses.

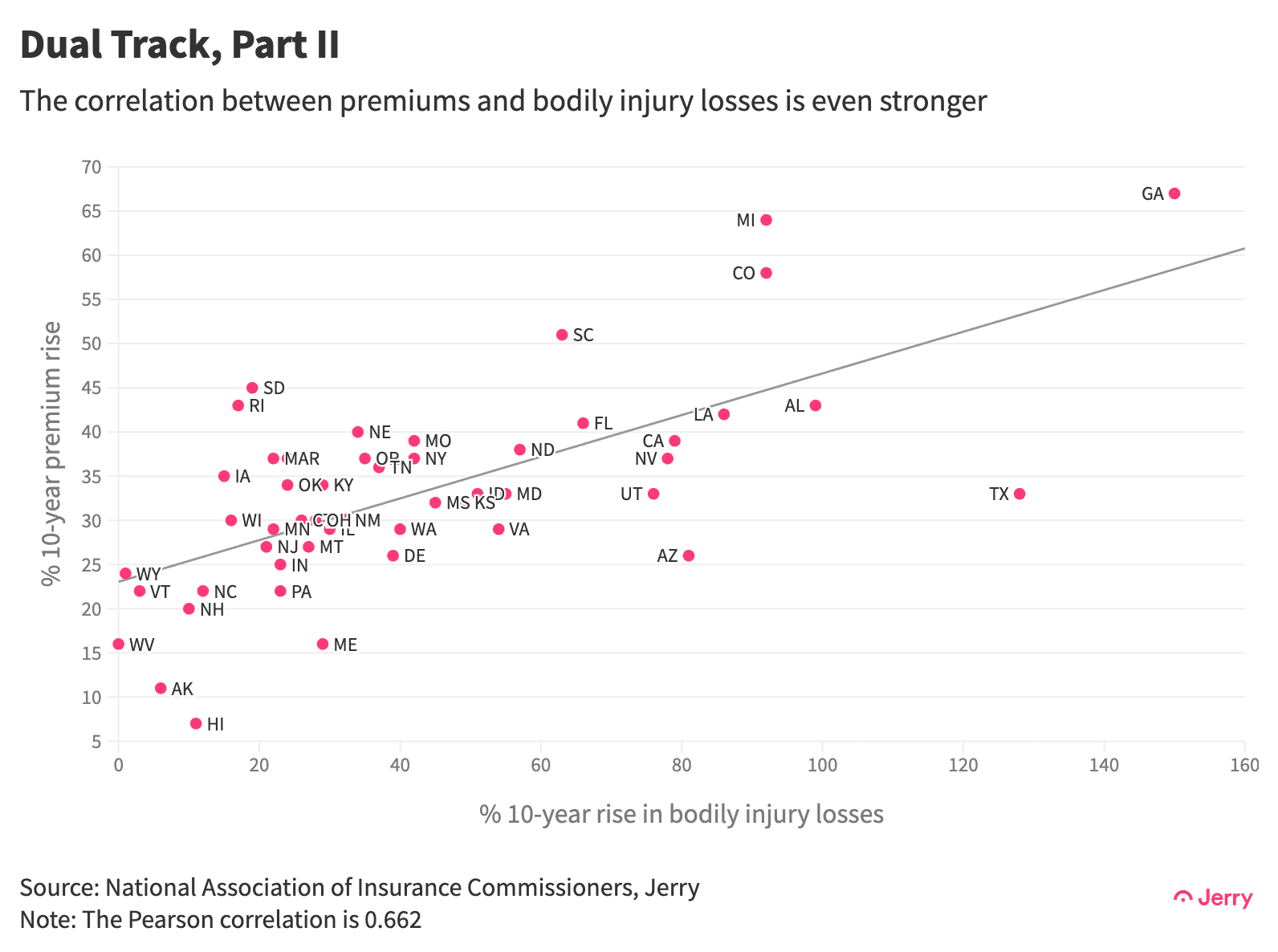

Data collected from the statistical agents and certain states by the NAIC illustrates that the dollar value of losses from claims has jumped. Total liability losses hit $99 billion in 2018, the latest year for which data was available, an increase of 50% from a decade earlier. Bodily injury claims rose 56% over 10 years to $39 billion, and collision claims jumped 48% to $41 billion.

Plotting those losses versus the increases in state premiums shows a positive correlation between them.

The correlation between the increase in bodily injury losses and rising premiums at the state level is even stronger.

Conclusion

Rising insurance premiums can be a painful fact of life even for people with spotless driving records. Yet data clearly show that the cost of covering auto claims is rising nearly as fast as premiums, indicating that driving habits and price increases for certain claim-related costs should, at least, get most of the blame for higher premiums overall.

Methodology

For household spending on vehicle insurance and other items, Jerry examined data from the BLS’s Consumer Expenditure Survey by income quintiles. To estimate 2022 expenditure figures, we took the survey’s 2020 data, the latest available, and adjusted them based on the rate of increased spending overall on those items in consumption data for 2021 and 2022 from the Commerce Department’s Bureau of Economic Analysis. The income range $35,000 to $60,000 a year represents the second and third quintiles.

All state-level data on premiums and losses were taken from the NAIC’s annual Auto Insurance Database reports. The NAIC includes a number of different measures for premiums, depending on policy type. To determine the states’ average premium we chose the NAIC’s “average expenditure” data, which the NAIC described as “an estimate of what consumers in the state spent, on average, for auto insurance.”

Data for total incurred losses from nationwide claims from 2012 through 2019 were taken from the Insurance Information Institute, which cited NAIC and S&P Global as sources. The rise in premiums over the same time period was taken from the BLS’s vehicle insurance index.

(This is an updated version of a study first published on Aug. 10.)