The used car market is headed back in the direction of normal but normal remains far away.

Wholesale prices, a leading indicator of retail prices, tumbled in the fourth quarter of 2022 and will likely drop further in coming months. And automakers are fixing the supply-chain disruptions that caught them flat-footed and decimated vehicle production, which

potential buyers of new vehicles into the used market.

But the disruptions of the past few years will reverberate through the used car market for at least several more years, as 1- to 3-year-old used vehicles, particularly those most in demand, remain scarce. This means that, barring a severe recession that destroys consumer demand, which looks increasingly unlikely, any downside for used car prices will likely be limited.

Key Insights

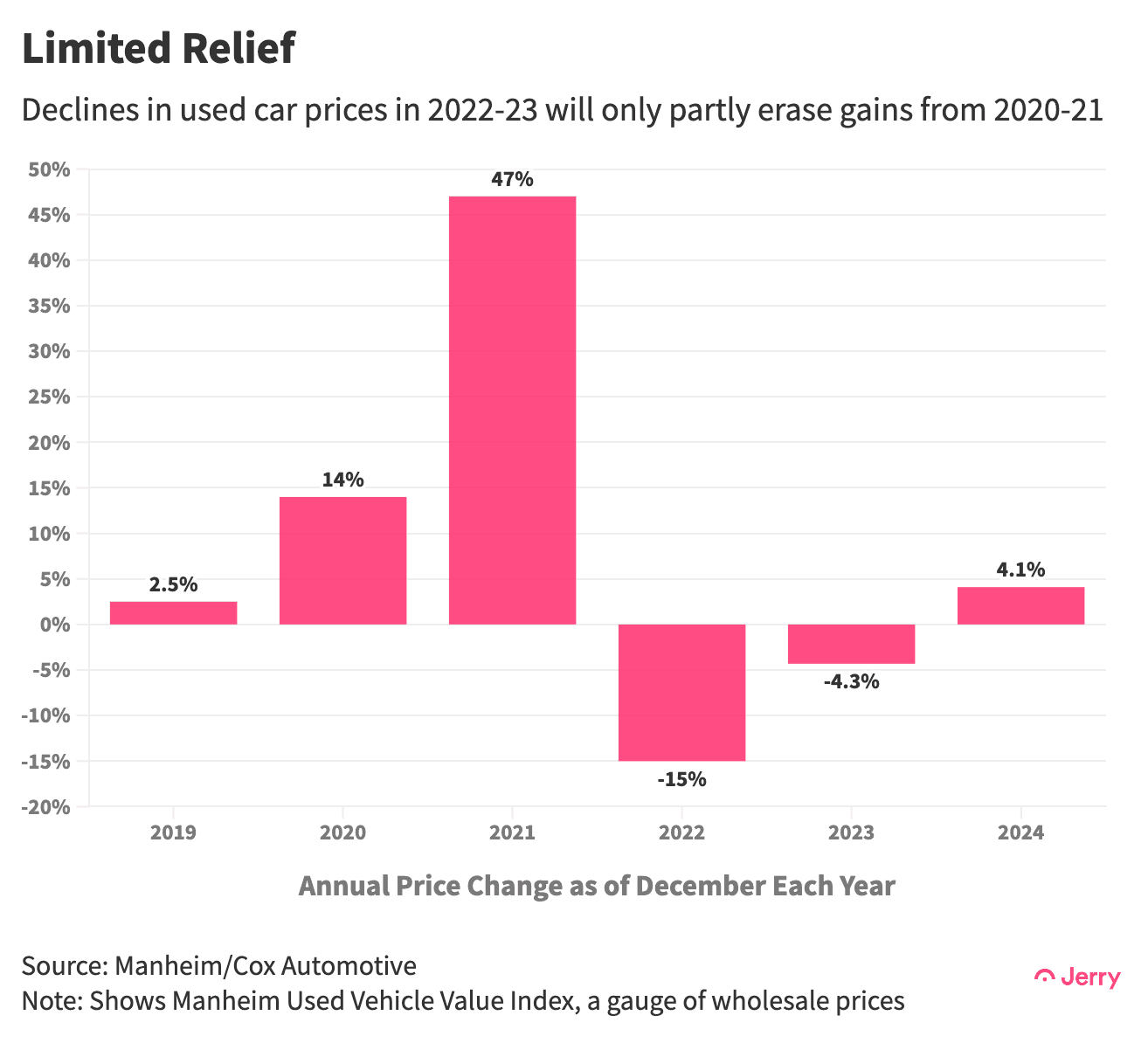

After a record-setting 15% decline in 2022, wholesale prices for used vehicles in 2023 will fall only 4.3%, according to analysts at Cox Automotive. Then prices will rise 4.1% in 2024 as the “extreme scarcity” of 1- to 3-year-old vehicles lasts for several more years, Cox analysts said.

Though the supply of new vehicles is recovering, a shortage of the types of semiconductors used in automobiles is still limiting vehicle production.

combined in 2021 and 2022, with another 2 million to 3 million expected to be scratched in 2023. Those are vehicles that would have hit the used market in coming years but now won’t.

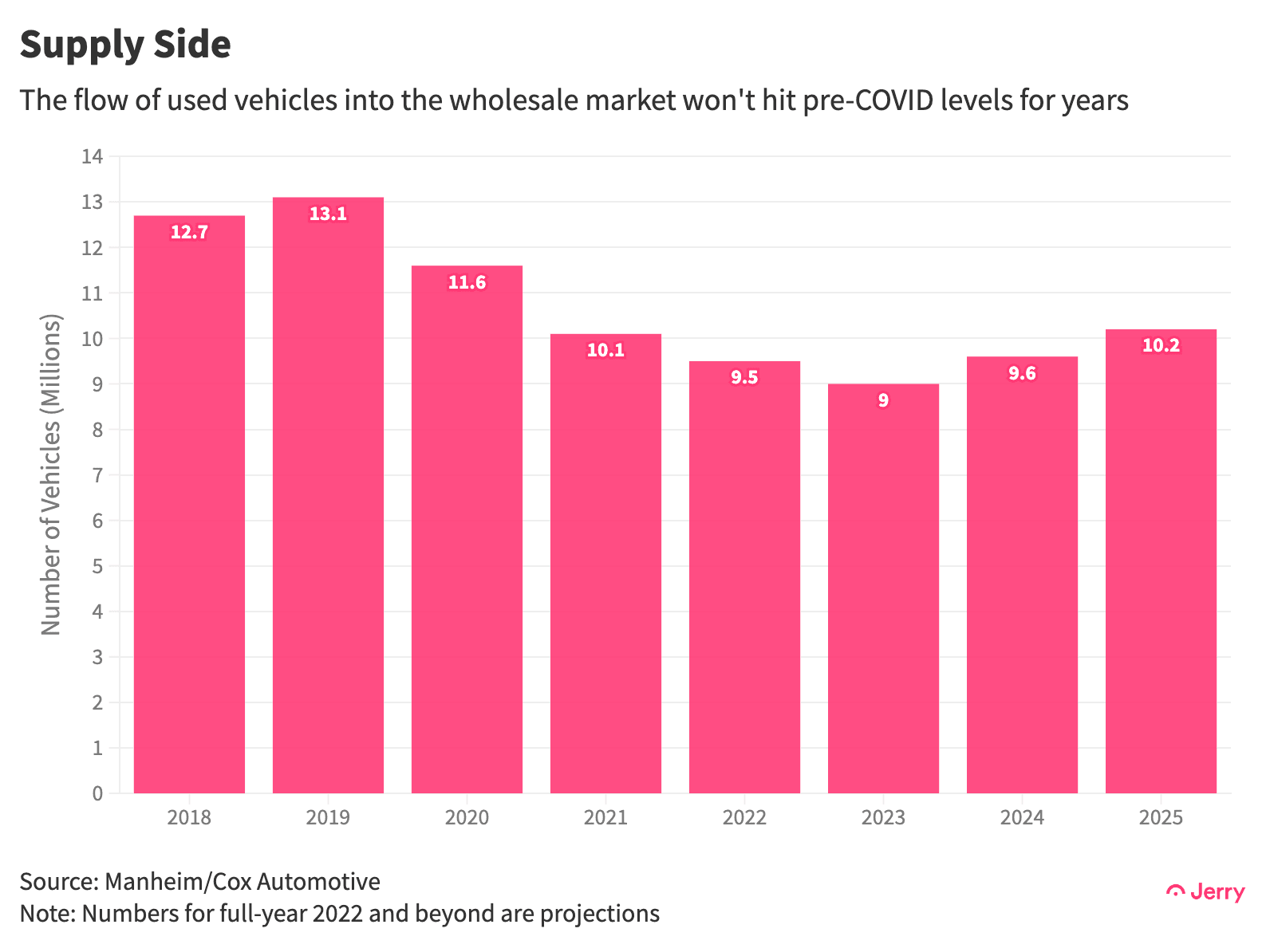

In 2023, the total volume of used vehicles expected to flow through the wholesale market to retailers and buyers is projected to be

, according to Cox Automotive. In 2025, it will still remain 22% lower, representing a shortfall of about 4 million vehicles that year alone.

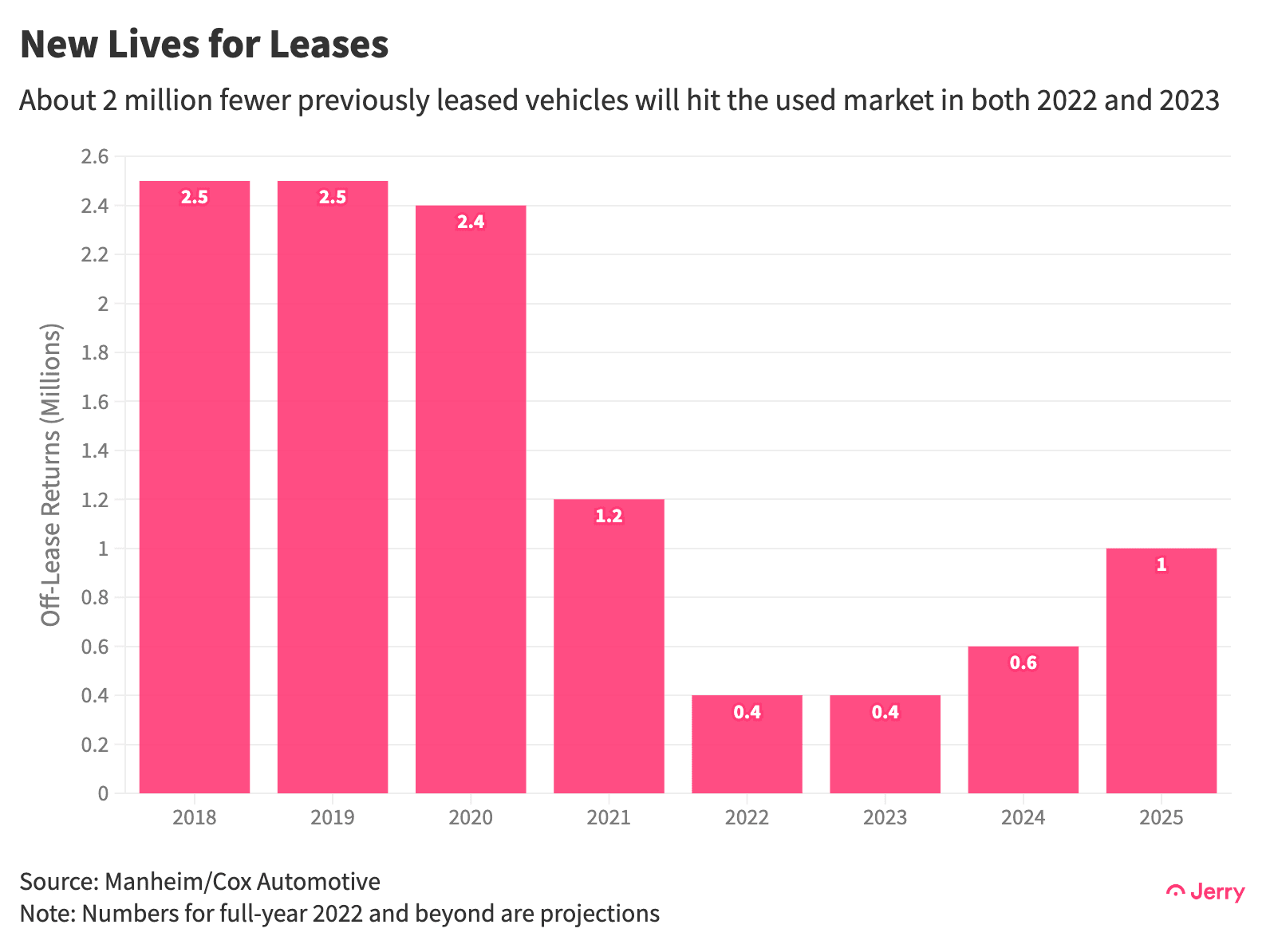

In 2022, the number of leased vehicles flowing to the used car market after the leases expired was estimated to have totaled only about 400,000. That’s 2.1 million fewer than in 2019, a decline of 84%. Roughly the same deficit is expected in 2023, narrowing only gradually through 2025.

The Chips Are Still Down

While many of the world’s post-COVID supply chain problems have been fixed, automakers find themselves in a tougher spot than, say, electronics companies. When automakers slashed chip orders at the beginning of the pandemic, fearing a collapse in demand for vehicles, most chip producers retooled their production lines to make more-advanced, more-profitable chips for electronics and other uses. When car sales unexpectedly came roaring back, automakers couldn’t find the chips they needed and were forced to cut production.

Nearly three years after the first COVID shutdowns in the U.S., automakers are still struggling to get all the chips they need. In recent months, some of the world’s biggest carmakers, including

, announced yet more production cuts. Softening demand for electronics may help free up some capacity for the types of chips that go into vehicles, but this would be a time-consuming switch, followed by a production process that itself takes months.

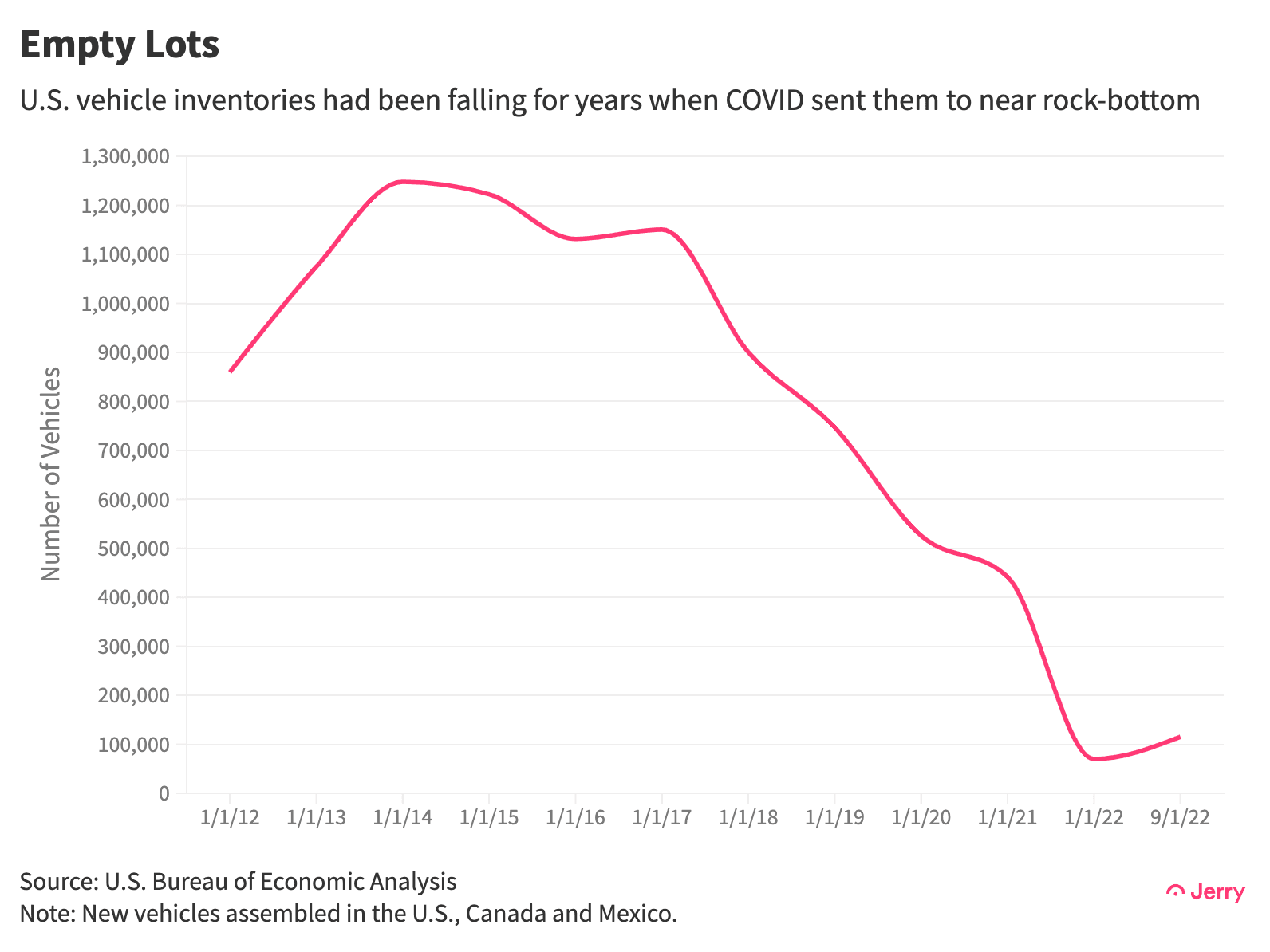

So output and inventories of new vehicles — which have been at historic lows for many months — will remain limited well into next year at least. Many

don’t see a return to a “more normal” supply of automotive chips until late 2024.

Pipeline Slows to a Trickle

Fewer new vehicles on dealer lots means more people will look to buy lightly used vehicles, 1- to 3-year-old versions of their preferred models. It also means that, eventually, fewer lightly used vehicles will flow into the used car market as trade-ins.

But the biggest single factor in the limited supply of lightly used vehicles is the near-total disappearance of previously leased vehicles from the used market. Prior to COVID, most people who leased vehicles declined to exercise their right to purchase them when their leases expired. But soaring prices for lightly used vehicles changed their calculus.

Previously, someone returning a lease usually found the vehicle was worth $1,500-$2,000 less than the previously agreed post-lease purchase price, according to analysts at Cox. But in 2022, vehicles built in 2019, for example, were worth $5,000-$9,000 more at the end of a 36-month lease than the agreed purchase price. So the vast majority of people are executing their purchase options, depriving used car lots of about 2 million vehicles in both 2022 and 2023.

Still, prices are expected to fall further in the first half of 2023 before stabilizing around mid-year due to pent-up demand and a severe shortage of 1- to 3-year-old vehicles, according to Cox analysts. Prices will fall 4.3% in 2023 before rising 4.1% in 2024, they said. That means buyers seeking better deals should wait at least until spring before shopping in earnest.

Conclusion

The incredible bull market for used cars has likely peaked as new car production recovers and demand softens due to higher prices and interest rates. But there will be a shortage of 1- to 3-year-old vehicles for years to come. This will keep a floor under prices, particularly for the most popular models. That’s likely to provide some relief for people who have bought such a vehicle in the past few years. Not so much for those shopping now or in the next few years.

(Note: This is an updated version of a study first published in November 2022.)