The slide in used car prices is just about over as the COVID-19 pandemic again roils car markets after three years of nearly unrelenting bad news for buyers.

Used vehicle prices started dropping at the end of last year and were expected to fall modestly this year, after a historic and punishing run-up over the previous two years. But declining inventories of used vehicles and a

in the new car market are combining to keep used vehicle prices elevated, according to analysts at Cox Automotive. They now see used prices rising in 2023, after previously forecasting a decline of 4.3% for the year.

Key Insights

Used car prices are expected to rise 1.6% this year, according to Cox Automotive, which previously predicted a decline of 4.3%.

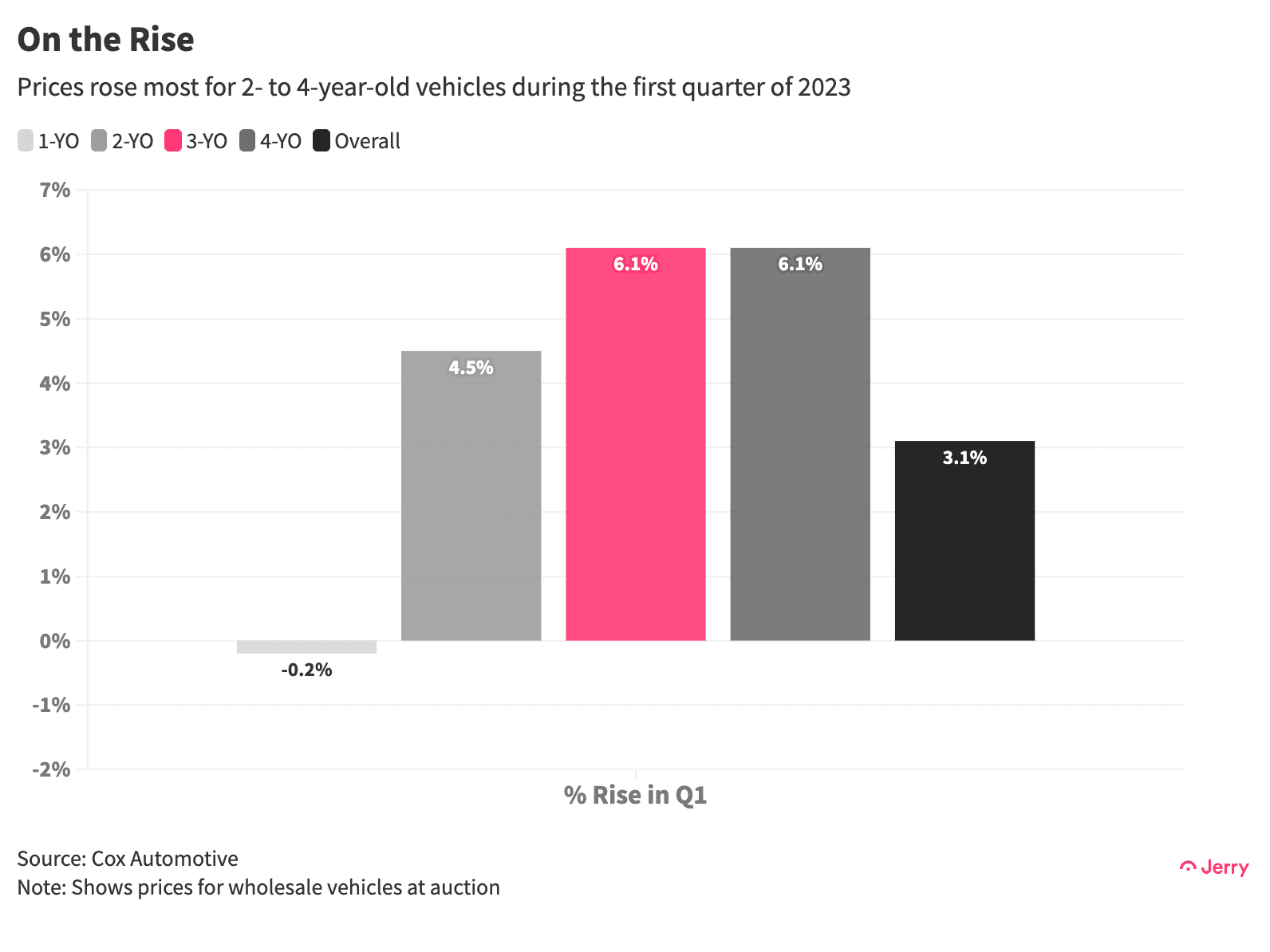

Prices for 3- and 4-year-old vehicles have risen 6.1% already in 2023, as more buyers abandon the new car market in search of lightly used vehicles.

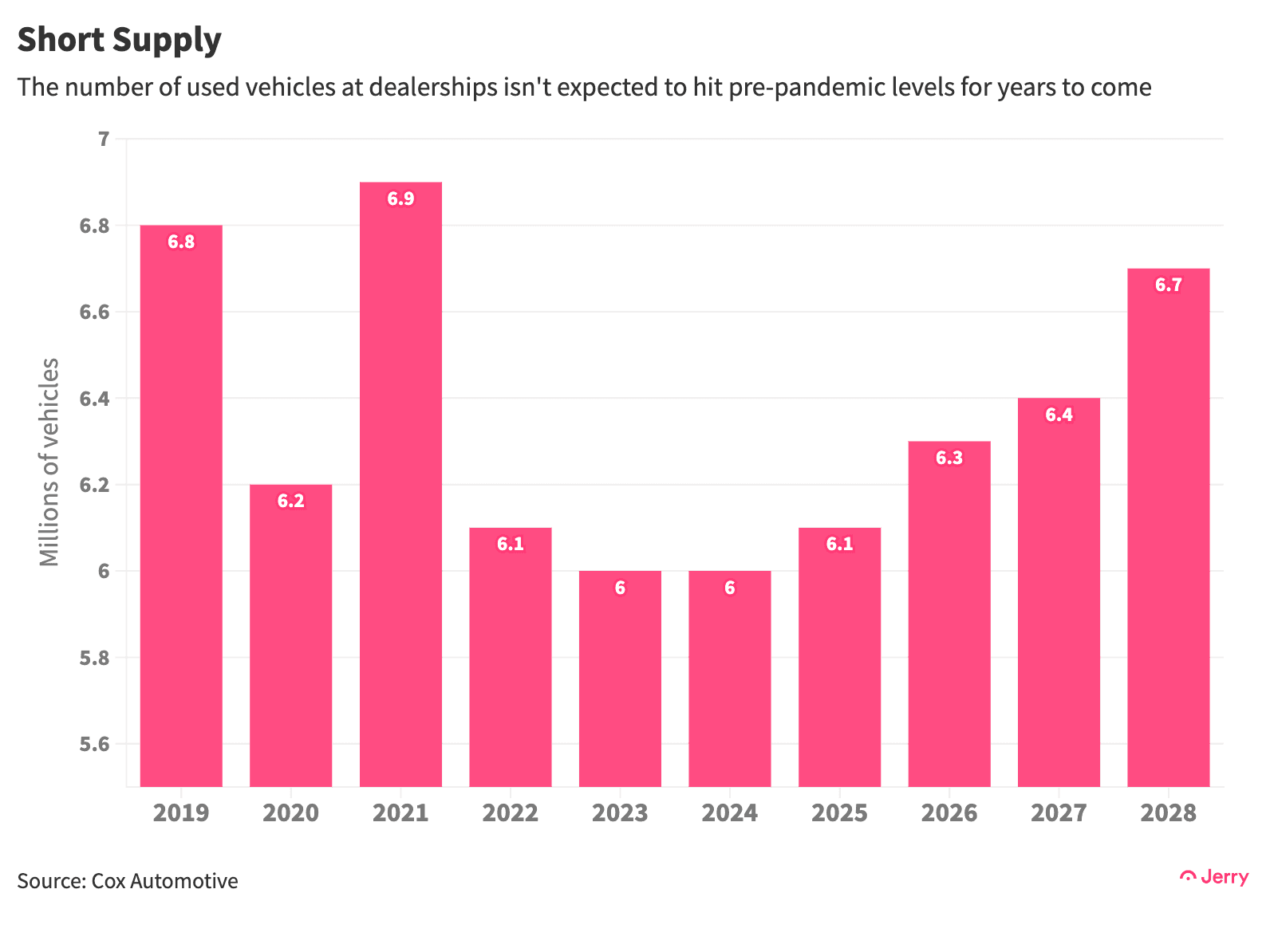

Inventories at used car dealerships won’t return to pre-pandemic levels for at least five years, according to Cox.

Used car prices are still lower than they were a year ago but the gap narrowed to only 2.4% in March. And by the end of the year it will be completely erased. Prices have been rising since the beginning of 2023, especially for newer models which are most in demand. Prices for 3- and 4-year-old vehicles rose the most (6.1%) in the first quarter.

Pandemic Production Cuts

On its face, the 1.6% increase that Cox has forecast for its Manheim Used Vehicle Value Index this year appears modest. (The index tracks wholesale prices, which are a proxy for retail prices.) But given the increase in prices of more than 50% from mid-2020 through early 2022, to many Americans it will feel like the pandemic is piling on.

When the pandemic hit, supply-chain disruptions forced automakers to cut production, depriving dealers of millions of new vehicles and pushing millions of buyers to the used car market. This sent used car prices spiraling higher,

Just as output and inventories of new vehicles are recovering, the early pandemic-era production cuts are disrupting the used market in a new way. Usually, most fleets and leases are returned to dealers when the vehicles hit three years old, providing the used market with a steady supply of relatively new vehicles. Any 3-year-old vehicles this year were made in 2020, the first year of the pandemic. There are a lot fewer of them.

Fleeing New Car Prices

Making matters worse, the affordability crisis in the new car market is spilling over into the used market. The price of new vehicles has risen 50% over the past 10 years, hitting a record $49,500 at the end of 2022, when the average car payment reached $694, roughly 12% of the after-tax median household income.

While prices of new vehicles have fallen slightly this year, they become unaffordable to more and more Americans each year, particularly after interest rates hit the highest level in 15 years. As a result, many people who previously would have been able to buy a new vehicle are now looking for “near-new” or 1- to 3-year-old cars, putting more pressure on an already tight used market.

Conclusion

With the used vehicle supply crunch expected to last for years, prices are likely to remain uncomfortably elevated for some time. Automakers would have to start producing a lot more cars, and inflation and interest rates would have to fall sharply, for the new car market to return to something resembling a pre-pandemic normal, which would take pressure off the used market. But automakers may have decided they don’t