The end of the years-long era of tame inflation and low interest rates has generated a crisis of affordability that has left new cars out of reach of many Americans.

In the years before COVID-19 struck, mild price increases, low interest rates and ever-lengthening repayment periods for

changed all that, putting a new vehicle out of reach of more and more people.

Jerry's charts below illustrate some of the key developments in this new normal.

Price Spike

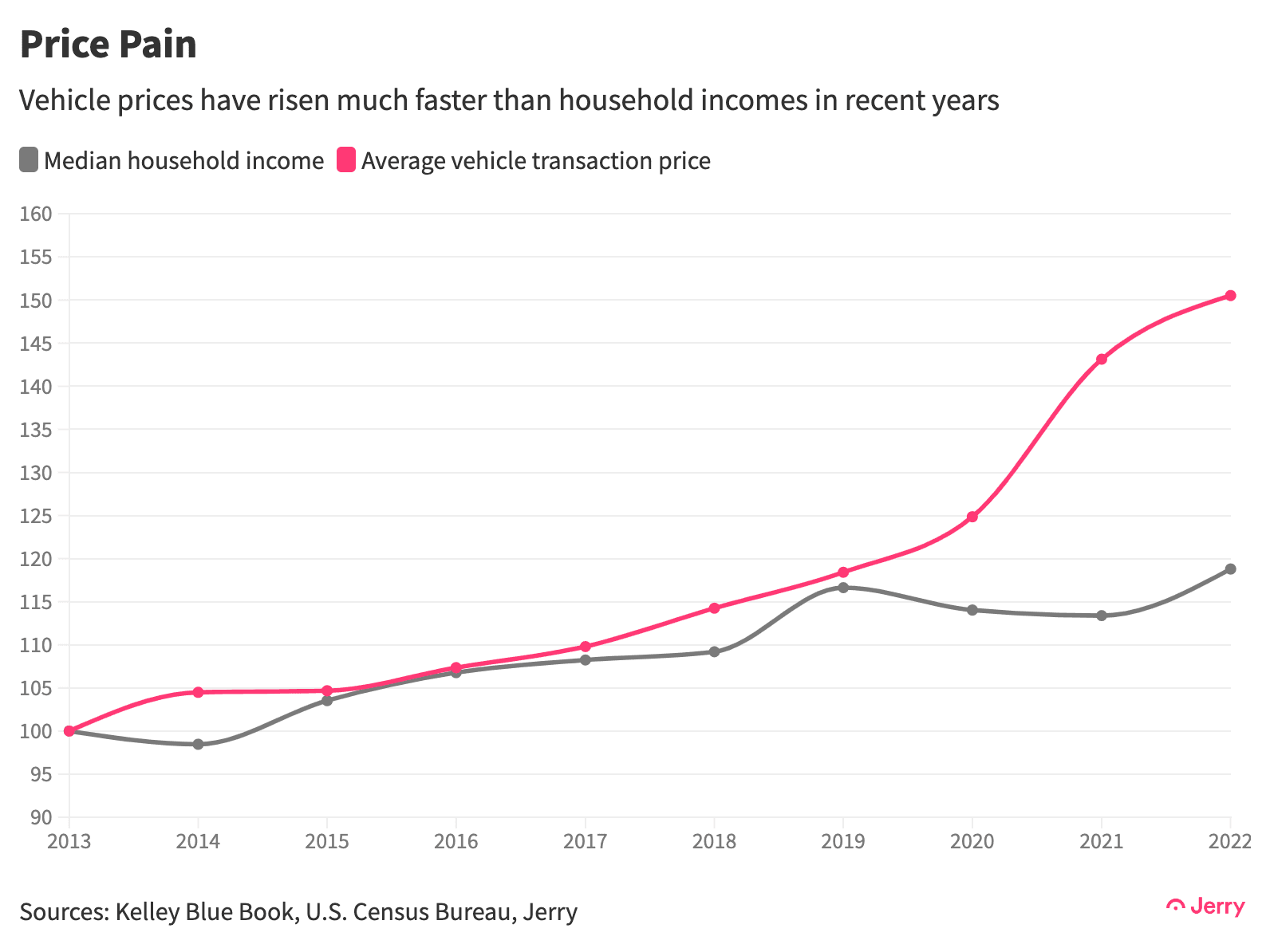

The average price of new vehicles has risen 50% over the past 10 years, hitting a record $49,500 at the end of 2022. That’s 66% of the median household income, which has risen only 19% during the same time. At the end of 2022, the average car loan payment was $694, roughly 12% of the after-tax household income.

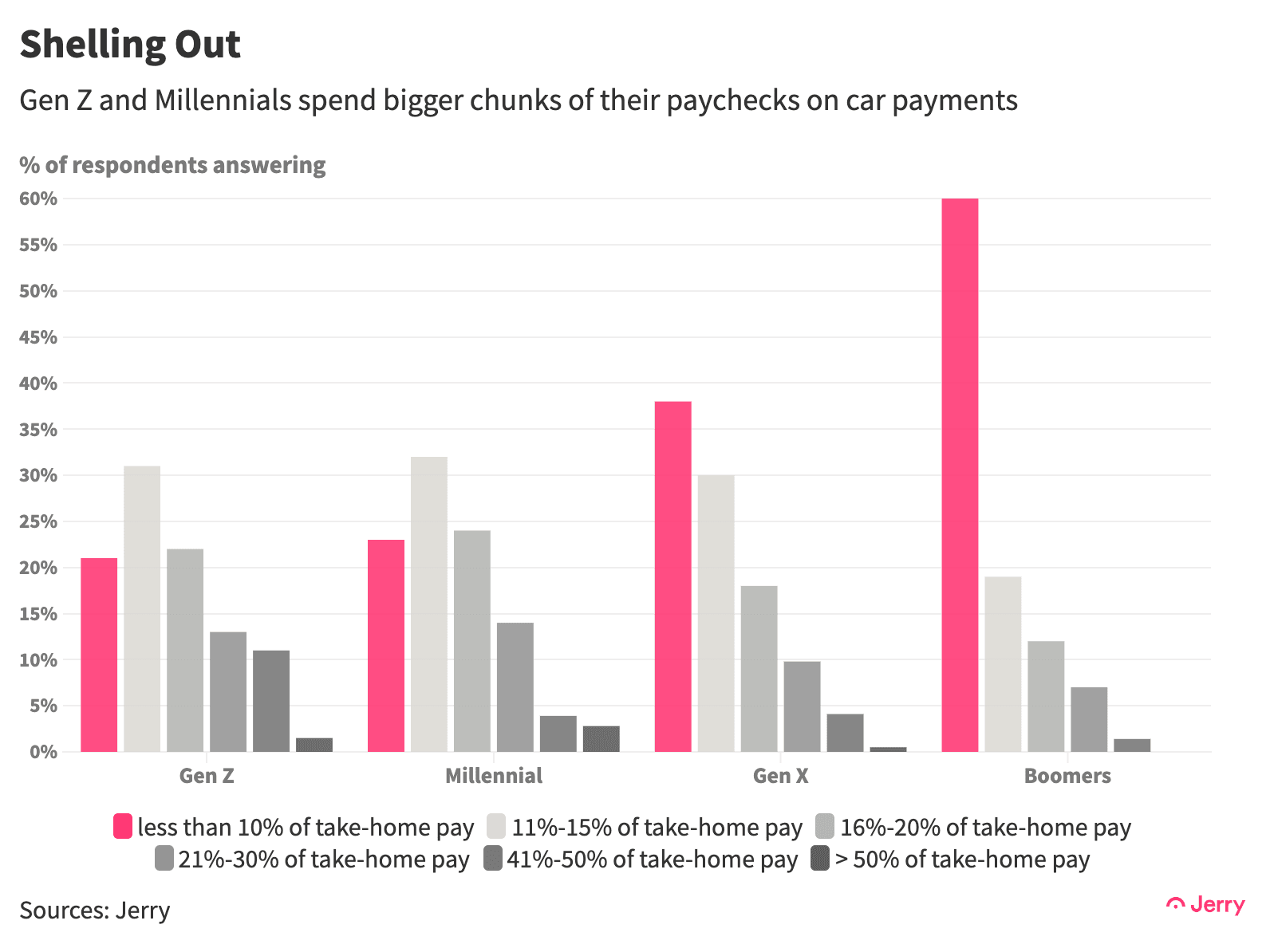

Many people, of course, are paying a far bigger slice of their take-home pay toward their car payment, especially Millennials and members of Gen Z. Last year nearly a quarter of American drivers

of their after-tax household income on car loan or lease payments and one in 10 paid more than 20%.

Supply and Demand

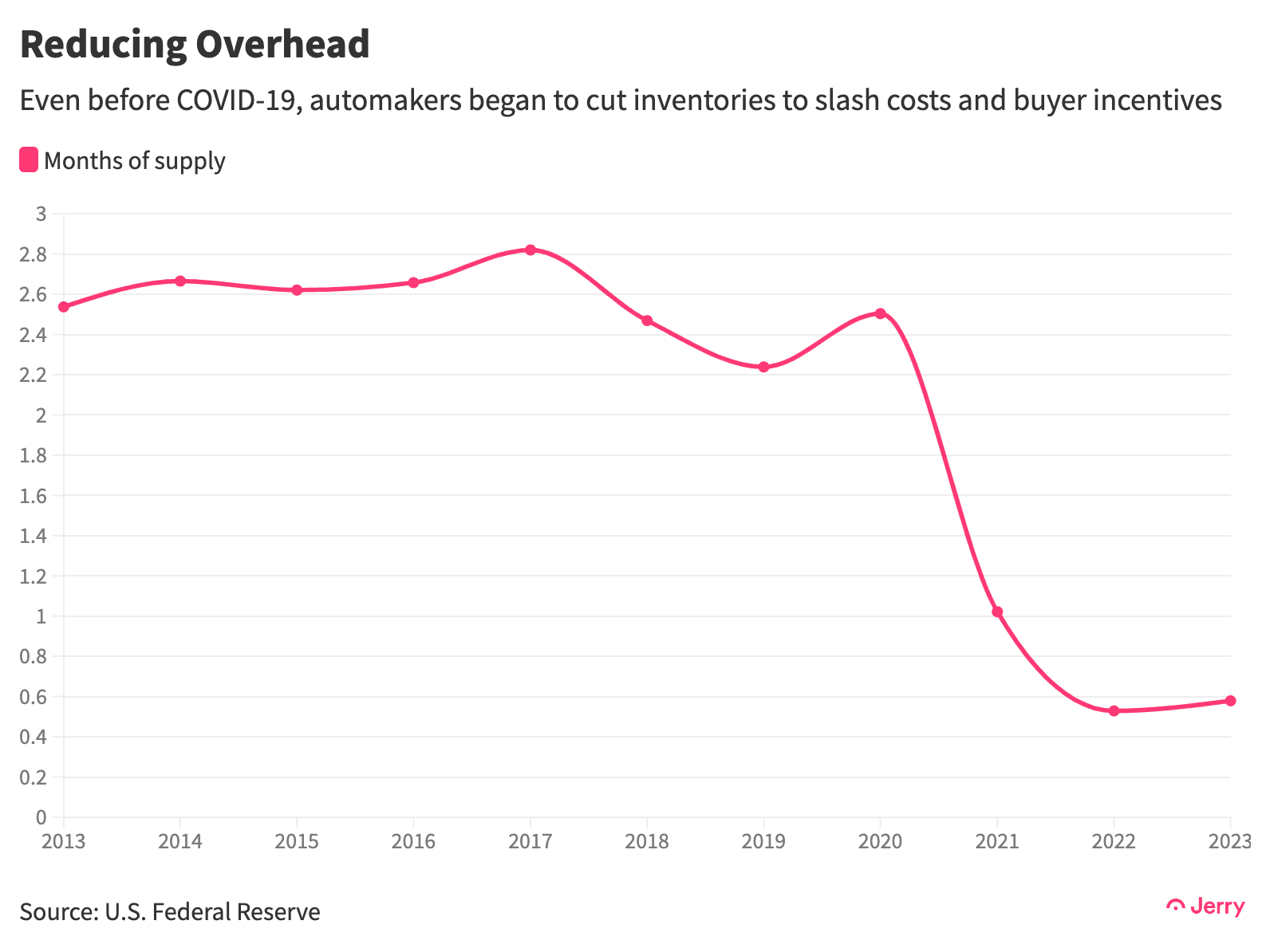

A supply shortage can be a good problem to have if you control the supply. Even before the pandemic, automakers had begun focusing on producing more expensive, higher-margin vehicles to boost profits. (In January 2023, luxury vehicles made up a record share of total sales at nearly 20%, according to Kelley Blue Book.) Automakers also cut production and inventories to reduce costs and avoid the need to offer aggressive incentives to buyers to clear dealer lots at year-end.

In late 2019, before COVID struck, the supply of vehicles on hand had already hit the lowest level since the height of the global financial crisis. After COVID, the supply disruption enabled dealers to charge eager buyers prices that were well above the Manufacturers Suggested Retail Price (MSRP).

Now the inventory-to-sales ratio is at the lowest level on record in data going back 30 years and some automakers,

, say they don’t plan to return inventories to pre-COVID levels.

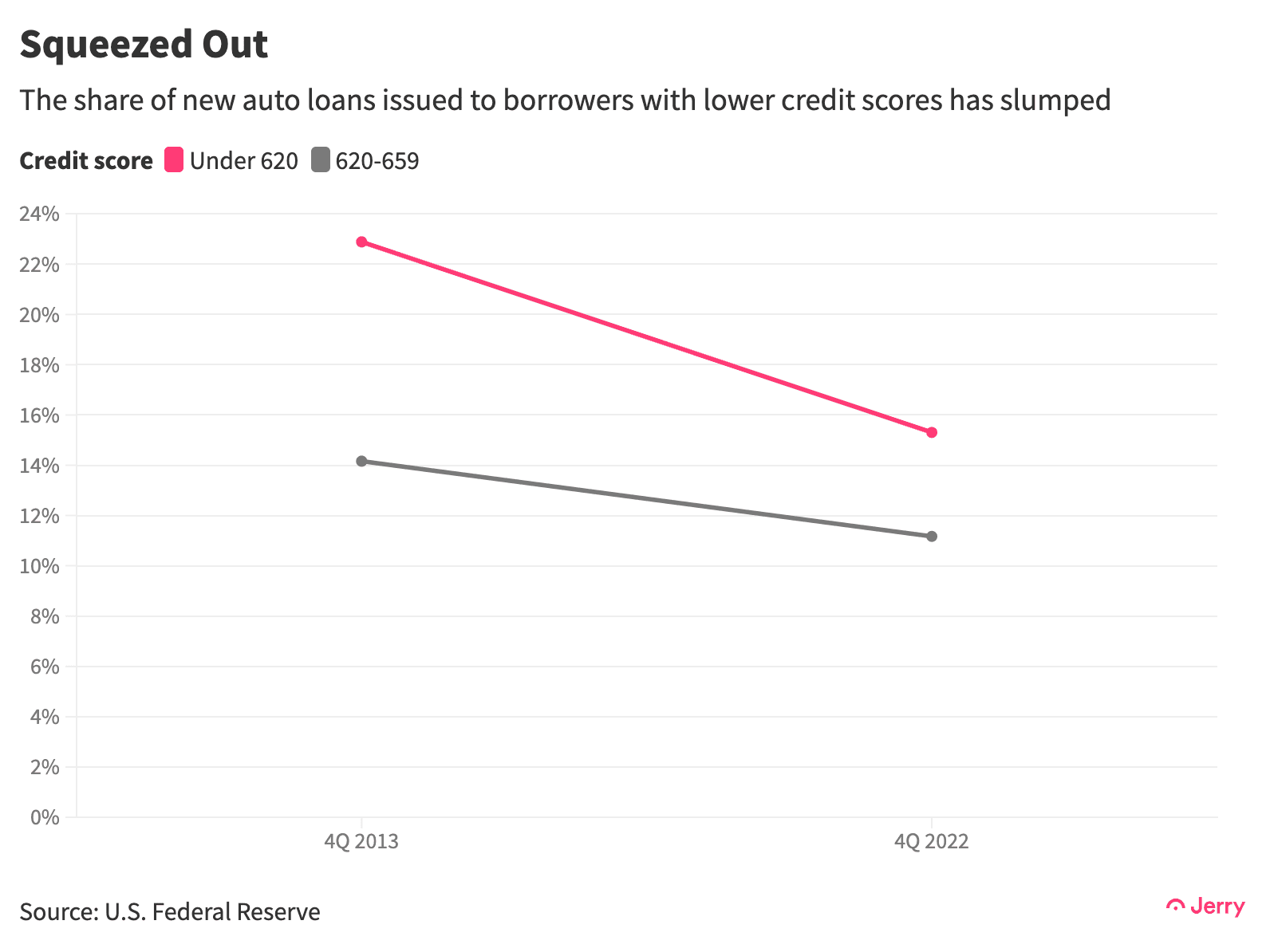

Rattled by the global financial crisis and, later, rising delinquencies on auto loans, banks and finance companies tightened lending standards on auto loans. The result has been that people with lower credit scores have found it harder to get them, as illustrated by their shrinking share of the market. Many so-called “subprime” borrowers are effectively being pushed out.

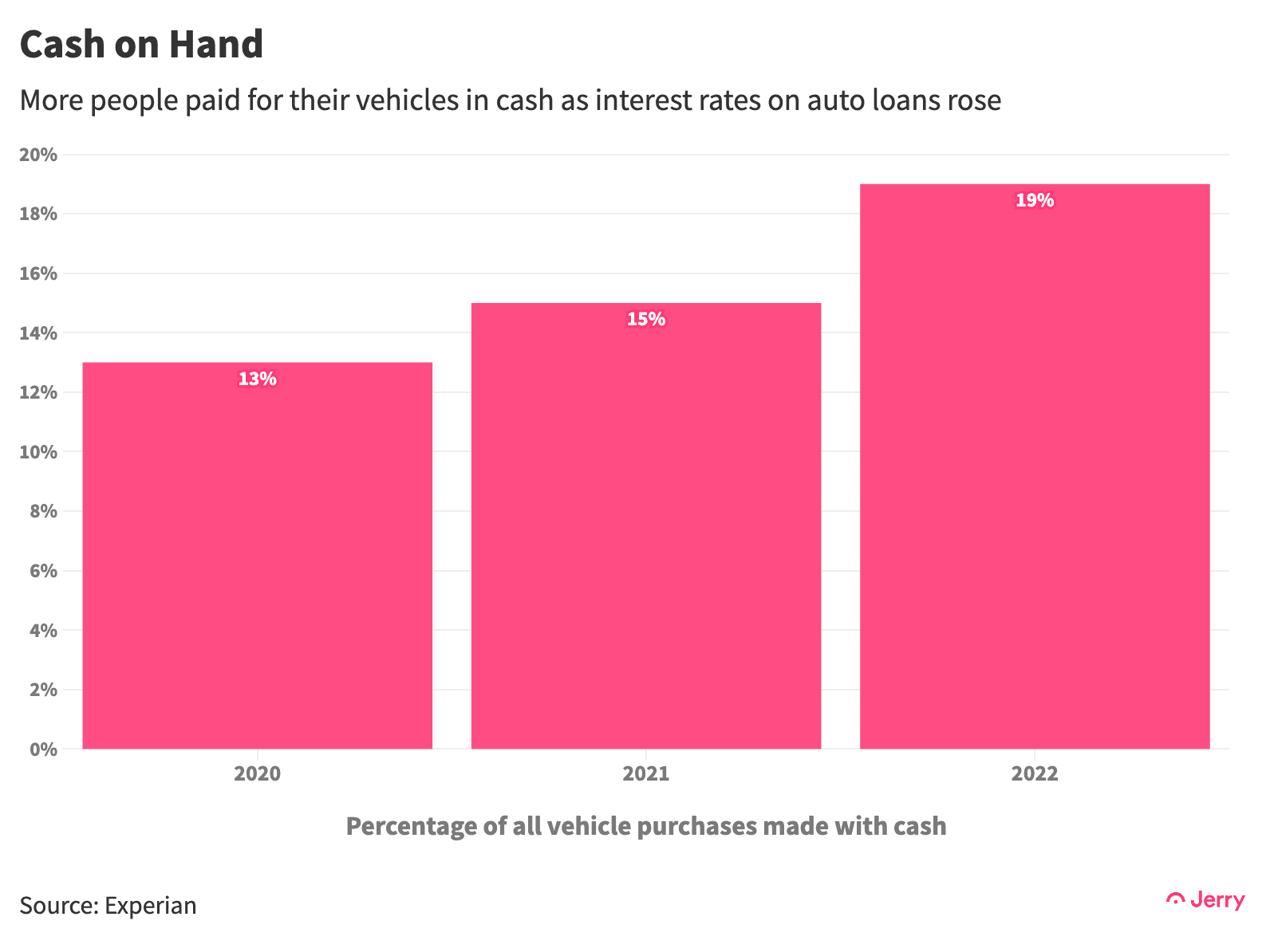

On the other hand, sales of luxury vehicles have surged, hitting a record high as a percentage of all sales. All-cash purchases have also hit long-term highs. The percentage of cash deals historically has remained below 15%, according to analysts at Cox Automotive, but the number of such deals has surged over the past two years, averaging 20% over the last three months of 2022 as interest rates hit

. The percentage of all-cash deals will likely hit a multi-decade high in 2023 as those buyers with means look to avoid paying higher rates on auto loans, according to Cox analysts.

Conclusion

Automakers appear to be comfortable producing fewer cars at higher profit margins. That’s not likely to change anytime soon, especially given a possible economic recession ahead. The Fed is still struggling to deliver a decisive blow to inflation, meaning there is no end to higher interest rates in sight. Which is to say, the average American will struggle to afford a new car for the foreseeable future.

Methodology

To calculate the average monthly loan payment, we used Census Bureau data on after-tax median household income and Federal Reserve data on average amount financed, loan length and interest rates for auto loans at finance companies.